Thoughts on Lemonade (NYSE: LMND)

17-Apr-23

The Elevator Pitch

I take a neutral view on LMND in cognizance of a well-balanced bull and bear debate on the stock that translates into a risk to reward of 1 : 1.4. To be clear, I like LMND as a Insurtech disruptor and its long-term growth story. I take a long view on LMND as an underappreciated and misunderstood stock positioned in a nascent TAM backed by a solid secular growth story with visibility on path towards profitability and a proven track record of management execution. However, present day risk on the stock remains material that translates into 35% downside from current levels – (1) Weak underwriting ability could undermine LMND’s path to profitability and (2) Cash burn pressure on balance sheet – hence my neutral stance on the stock. I’m valuing LMND on 4x 1-Year Forward P/S with a target price of US$20.80, +50% upside from 7-Apr-23’s closing price of US$13.84.

My Thesis

LMND is an underappreciated and misunderstood stock positioned in a nascent TAM backed by a solid secular growth story with visibility on path towards profitability.

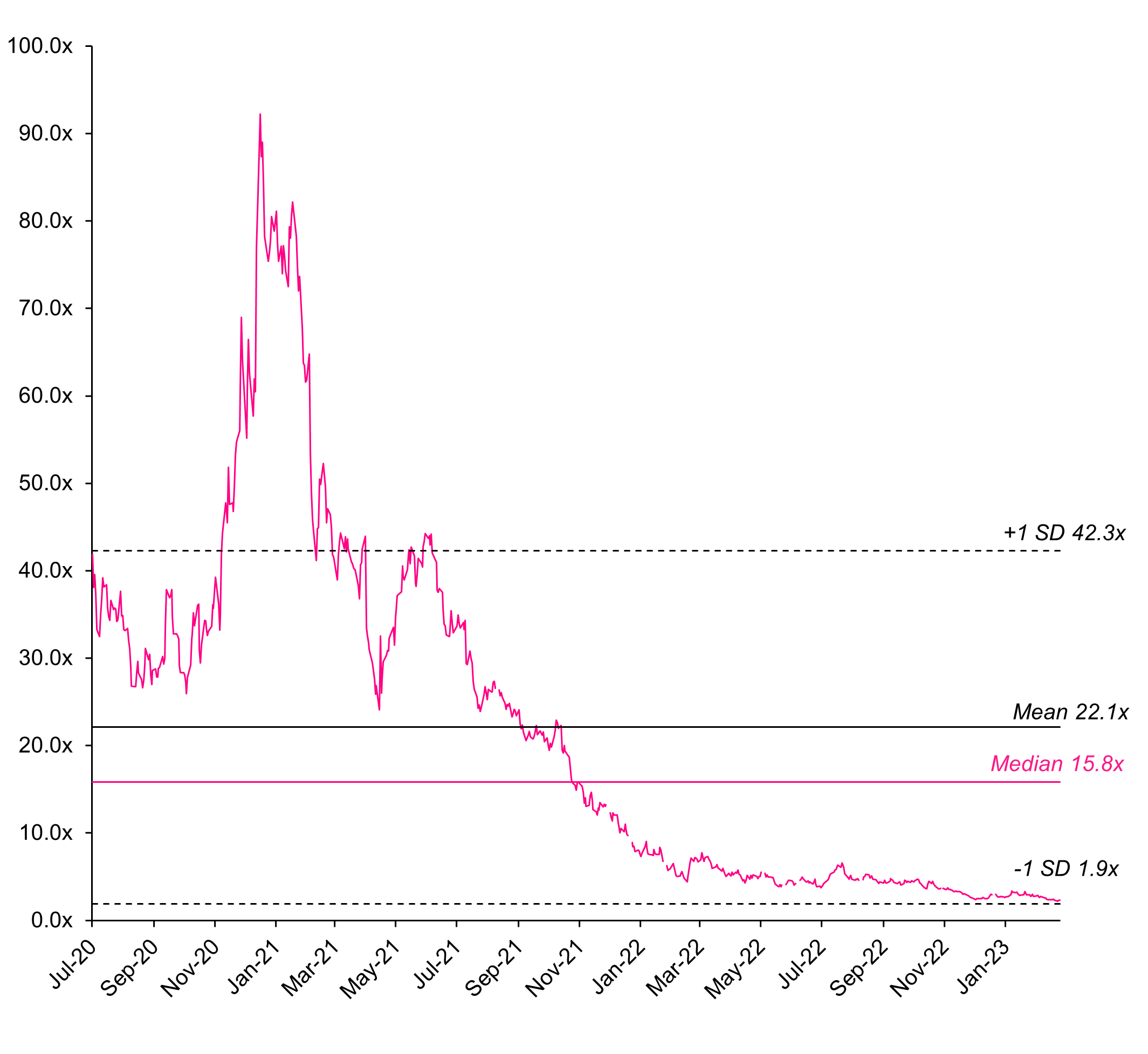

LMND is down 80% from listing (2-Jul-20) to date (9-Apr-23) due to a mix of fundamental and macro reasons. On a macro level, rate hikes, inflation and recessionary fears led to a series of selloffs in 2021 and 2022. On a fundamental level, rise in loss ratio from entry into new markets and aggressive customer acquisitions in FY22 has led to unprecedented cash burn levels. Concerns on visibility and path towards profitability has severely punished the stock with LMND now trading at 2x 1-Yr Forward P/S.

The street views LMND as a typical hype stock positioned in a secular growth industry with high cash burn, replicable competitive advantage, and a bleak path towards profitability. While I acknowledge that LMND’s cash burn run rate raises eyebrows on its balance sheet, I think the stock is misunderstood by investors and I take an opposing view from the street.

Firstly, LMND’s AI competitive advantage is not easy to replicate as incumbents lack the same systems or technical folks, and often have legacy systems built on monolithic and dated code. Incumbents are maladaptive in going up against Insurtech disruptors due to vast networks of brokers, decades of cumulative investment in disparate IT systems, corporate cultures adapted for legacy preservation rather than business transformation, and policy-centric rather than customer-centric organizations.

Secondly, sellside views tend to downplay and underappreciate LMND’s up and cross sell strategy. LMND focuses on customers that are initially unattractive to the incumbents due to inability in purchasing big ticket items insurance products. It is only when these customers graduate from small ticket items into big ticket items that the incumbents start eyeballing these customers. However, switching cost and user-stickiness is likely to accumulate over time in driving these customers to graduate into big ticket item insurance buyers with LMND rather than switching over to incumbents such as Geico and State Farm.

Thirdly, the debate on LMND’s “minimal path towards profitability” can be demystified by the front-loaded cost nature of an Insurtech firm. LMND is front loaded in its expenses with bulk of costs being upfront, coming from product development and customer acquisition. This explains the high S&M as a percentage of sales in the last two years. I see positive tone from management on turning profitable. According to FY2Q22 earnings call, “our leading indicators strongly suggest that the business we are underwriting today will prove profitable even if lagging indicators take a few years to fully reflect this.”

Why now?

LMND today has reached an inflection point on cash burns and losses as management switch gears from end-market expansion and aggressive customer acquisition to (1) cross and upselling, and (2) improving loss ratio via elimination of mispriced customers and non-renew unprofitable business in paving the way for profitability. Meaning to say, gross loss ratio should start to contract meaningfully, intensive cash burn should start subsiding and net loss should start narrowing down. LMND is now well on track towards profitability by FY25/26E.

Bridging narrative to numbers, I expect LMND to grow at >30% CAGR on topline in FY23-27E driven by the disruption story. Management provided medium term targets on the recent analyst day where they expect in-force premium to grow at 20% CAGR in FY23-27E, gross loss ratio to come down from 89% today to <70% by FY27, and for up/cross sell rate (multi-line customer rate) to expand from 3.7% today to >25% by FY27. Going by these numbers, LMND should turn profitable with positive FCF in FY25/26. Importantly, LMND’s management has demonstrated credibility given their track record of meeting or beating the past 10 consecutive quarters of guidance. I expect management to continue executing well and in meeting the medium-term targets.

How to think about valuation today

LMND’s valuation today is dirt cheap. At 2x 1-Year Forward P/S, I believe LMND’s stock has bottomed out with both fundamental and macro concerns fully baked into current stock price.

Current valuation is unjustifiably low today considering the growth momentum and path to profitability that is ahead of LMND. The high cash burn and unprofitable names within the software and ecommerce space are currently trading between 5-10x 1-Year Forward P/S. I reckon ~4-5x as a more reasonable multiple for LMND to trade on.

I value LMND on 4.0x FY23E P/S and arrive at a target price of US20.80, +50% upside from 7-Apr-23’s closing price of US$13.84.

(1) Internet, Software, and Payment players currently unprofitable with high cash burn

What’s gonna move the stock

Given management’s analyst day guidance and street’s concern on LMND’s cash burn and profitability, I expect LMND’s next 12-month stock price to be driven by

(1) Gross Loss Ratio

(2) IFP Growth

(3) EBITDA

Near term catalysts includes:

(1) Launch of insurance offerings into new states.

LMND currently offers their primary product of renter insurance in 42 states within US. Other insurance offerings such as autos, and pets has yet to be offered for most states. Expect stock to react from announcement of product offerings into new states. Stock has a tendency of reacting +10 to +15% whenever LMND launch their products into new states.

(2) Quarterly earnings reflecting meaningful improvement on key metrics.

LMND’s stock price moves on i) In-Force Premium growth, ii) Gross Loss Ratio, and iii) EBITDA. Improvements on these metrics in the next few quarters should garner positive sentiments from investors in driving rerate on valuation multiple. Gross loss ratio contraction by >400bps, IFP growth by >12%, EBITDA loss of < ($240) should drive positive reaction and pop the stock.

What if I turn out wrong

(1) Weak underwriting ability to undermine path towards profitability

LMND is a fundamentally weak underwriter given their net loss ratio. With no changes to fundamentals, the Street does not expect meaningful improvement on net loss ratio going forward despite management’s guidance. Underwriters, especially within commercial lines, have historically been at the nexus of these two forces: using judgement to balance speed and flexibility with thoroughness and precision. The application of technologies such as telematics, IoT, and AI has promised to deliver underwriting efficiency and accuracy simultaneously but, in practice, has often improved one at the expense of the other. I see possibilities of i) insolvency, ii) acquisition by incumbent, or iii) valuation going under 1x P/S should LMND fail to find a path towards profitability from weak underwriting abilities.

(2) Balance sheet stress from delayed path to profitability

Cash from balance sheet today can only sustain another 3.5 years of burn. Should LMND remain unprofitable beyond FY27, debt/equity raising will be required. Equity raising will bring about dilution on shares outstanding while debt raising will further lever LMND’s balance sheet coupled with bottomline impact from increased interest expense. Either approach will erode EPS. Valuation would likely derate. All in, a significant impact on stock price if LMND fails to turn profitable by FY27.

Risk to Reward

Should these risks materialize, I would expect valuation to remain depressed under ~2x P/S while shares outstanding widens by 10%. This translates into downside of 35% from current levels. This brings me to an overall risk to reward of 1 : 1.4, an evenly debated bull vs. bear story. I recommend to act on the stock only if risk to reward improves to a minimum of 1 : 2, or if FY23E results reflects a significant beat on guidance.

Company Overview

Lemonade (LMND) is a consumer-facing online insurance platform that provides insurance products to renters, condo owners and homeowners in 42 U.S. states, as well as in Germany, Netherlands, and France (licensed in 31 European countries). Apart from housing insurance, LMND also offers pet and car insurance. The company operates an app and website where prospective policyholders can receive a quote and buy insurance through a completely automated onboarding and customer experience bot. When a customer who purchased insurance wants to make a claim, the company’s automated claims bot handles first notice of loss 96% of the time and ~1/3 of all claims are resolved in a completely automated fashion.

The company generates revenue primarily from Premiums earned on written insurance policies, which range from $60 annual renters’ insurance policies at the low end to $1,000+ annual homeowners’ policies at the high end. The company recognizes revenue over the life of a policy, which are generally 1-year in length. Currently, LMND has a 89% loss ratio on its earned premiums, which largely reflects costs to pay out claims to policyholders. In 1H20, LMND started passing through roughly 75% of its written Premiums (and associated losses) to reinsurance partners, receiving a commission to do so.

LMND’s Value Proposition

(1) Offer insurance on a direct-to-consumer basis (DTC),

(2) To young insureds (~90% of its customers are first time insurance buyers),

(3) Using technology to eliminate and streamline costs (underwriting staff, claims staff, commissions, etc) that plague the industry,

(4) In a way that reduces tensions between the insurance company and insureds.

Total Addressable Market

On a sector level, according to market reports (Allied Market Research, Mordor Intelligence, Grand View Research), US Insurtech market is expected to grow at more than 50% CAGR from ~US$1bn in CY21 to ~US$45bn in CY30. This is primarily driven by proliferation in fintech infrastructures which laid a foundation for Insurtech players to offer cheaper insurance products with faster claims processing and policy administration. While it is hard to put an exact number on LMND’s TAM due to its niche offerings, we broke down its different end-markets (renters, autos, pets) and arrived at a ballpark of ~US$30bn TAM.

Renters market is small butb homeowners market is big. Combined, the home/renters market has a TAM of > ~$100bn. Renters is probably less than 5% of that total. LMND has also made initial footing in the property market in Europe (about €105b market). Between homeowners and renters, LMND currently skews heavily towards renters who on average pay significantly lower premiums. The company estimates that homeowners on average pay around 5x the amount of premiums that renters do with an average lifetime that is twice as long as renters. From a premium per customer perspective, AllState, one of the largest homeowners’ insurance companies in the US, generated an average Gross Premium Written of ~$1500 in 4Q 2022, compared to LMND’s < $250 overall in the same period. LMND’s most inexpensive policy offerings start at $300 per year in Homeowners and $60 per year in Renters.

The market is incredibly fragmented. Top-10 players have about 60% of the market. #1 (State Farm) is 18% of the market with > $18bn of premium, but it falls off fast after that. Beyond the top-10, no one has > 2% market share. Beyond the top-15, no one has > 1% share. LMND has moved quickly in this fragmented market.

Competitive Landscape

Key incumbents within LMND’s end markets includes Geico, Allstate, Amica, State Farm, Farmers Insurance, and Liberty Mutual. Consequently, LMND faces intensive competition in the homeowners and autos space given the lucrative market opportunity as compared to renters. While we expect some upselling in LMND’s renters to higher value policies over time, including homeowners, direct customer acquisition in the homeowner category will likely be challenging prior to reaching more meaningful scale (in ~3-5 years time). The incumbents trade at a 25-year historical average of 15-20x 1-Year Forward P/E.

LMND’s Value Proposition

The LMND app and website were first launched in late 2016, with the goal of bringing a mobile-first, low-touch solution to insurance for consumers and reduce the time between first query to bindable insurance quote. Today, the median time to get an insurance quote is under two minutes for renters and under three minutes for homeowners.

Onboarding Process: When customers first open the app or website, they have a conversation with AI Maya, a customer experience bot, that collects details relevant to a policy including address, apartment number, customer name, level of coverage desired, and other information. After AI Maya asks an average of 13 questions, generally a smaller number than legacy brokers, an annual policy (with monthly cost displayed) is generated with relevant insurance coverage information, and customers can set up a variety of payment options from Apple Pay to credit card. For renters, examples of coverage options include personal property, personal liability, loss of use, and medical payments in the event of injury.

Claims: 96% of first-notice of loss communications are done through the company’s claims bot, AI Jim. Customers fill out a claims report online or in the app, which can be substantiated with receipts, other documents, and even videos where a customer explains aspects of a claim. AI Jim handles the entire claim through resolution in one out of every three cases, while human interaction in the other 2/3 of claims is minimized by AI Jim’s up front capabilities. In the event of an approved claim, customers share wiring information to receive funds.

Technology: LMND’s ability to capture data points electronically through customer responses during onboarding, claim behaviour, policy ‘graduation’ behaviour, and other touch-points in the insurance process, in conjunction with the company’s machine learning capabilities, has allowed the company to more easily detect fraudulent claims over time and avoid losses that it previously might have paid out to customers. In addition to what this has done for loss ratios and appropriate policy pricing, the company has automated real-time tracking of potential catastrophes like severe weather events to appropriately course-correct policy pricing approval where needed.

At price points that are generally at the lower-end of the market and in a category that is small by incumbent insurance standards, LMND has been able to effectively capture insurance spending from renters, particularly in urban areas, that are early on in their experience with renting or owning property.

LMND’s forward strategy relies: 1) on further penetrating the renters’ insurance market through customer acquisition; and 2) ‘graduating’ early renters’ cohorts to higher monetized products, like homeowners insurance, condominium insurance, or pet insurance, as these customers get older and have more disposable income to purchase primary residences, purchase secondary residential properties, and own pets. Importantly, LMND notes that 70% of current customers are under the age of 35 and 90% of customers did not switch over from another carrier, indicating that the firm is expanding the renters’ market and acquiring customers earlier in their insurance lifecycle.

Today, however, LMND doesn’t participate in a meaningful segment of the homeowners insurance policy market, particularly with regard to higher value properties and with requests beyond a certain coverage level, which we believe is limiting their ability to break into the market more meaningfully but is likely crucial to maintaining the loss ratio improvement the company is seeing.

LMND focuses on younger/first-time insureds with low current insured value — 90% of customers are first-time insurance buyers. However, as customers age and undergo life cycle changes, their insured value increases; for example, they may upgrade to a homeowners policy from a lower-cost renters policy. LMND focuses on these customers before they are attractive to incumbents, and if the company is able to retain their business over time, company's top line benefits from their increasing insured value

Key End Markets

(1) Renters and Homeowners Insurance

The renters and homeowners insurance covers stolen or damaged property, and personal liability, which protects customers if they are responsible for an accident or damage to another person or their property.

(2) Pet Insurance

The pet insurance covers diagnostics, procedures, medication, accidents or illness. LMND also offer two optional add-ons to the basic plan, a wellness package and an extended accident and illness package. These provide additional coverage for preventative care costs, including annual exams and vaccines, and recovery treatments, including physical therapy and hydrotherapy. In Oct-22, LMND established a strategic partnership with Chewy, an American online retailer of pet food and pet-related products, in offering LMND pet insurance to its 20mn online customers. According to industry reports, the pet insurance TAM in US and EU stands at ~US$5bn today and is expected to grow at 15% CAGR in FY23-27 to ~US$11bn, driven by growing pet population, adoption of pet insurance in underpenetrated markets, increasing veterinary care costs and humanization of pets.

(3) Autos Insurance

The car insurance covers car accidents, weather damage, theft and vandalism, damage from external environment, liability for bodily injury, property damage, and medical expenses. In Jul-22, LMND completed the acquisition of Metromile in competing in the autos insurance space.

The Metromile Acquisition

On 8-Nov-21, LMND entered into a definitive agreement to acquire Metromile. On 28-Jul-22, LMND closed the acquisition of car insurance provider Metromile. Metromile shareholders received 7.3 million LMND shares, while LMND received a business with over $155m in cash, over $110m in premiums, an insurance entity licensed in 49 states, and a team unsurpassed in harnessing precision data for auto insurance.

Metromile is a tech auto insurance player where it uses individual driving data to calculate premiums. Historically, actuaries have relied on group-based statistics like age, gender and marital status to determine behind the wheel risk. Lack of individual data means that low risk customers are generating most of the profits and subsidizing the high-mileage drivers. The company estimates that 65% of drivers are “overpaying” relative to their risk.

Metromile offers real-time, personalized auto insurance policies by the mile instead of the industry’s reliance on approximations that have historically made prices unfair. This digitally native offering is built around the modern driver’s needs, featuring automated claims and complementary smart driving features.

Metromile attracts customers through a simple operating model. Customers receive a set base rate and per mile rate based on demographic factors and type of vehicle (up to 6 cents a mile). A small free wireless device called Pulse plugs easily into their car and the company uses telematics devices to track mileage only.

Acquisition Rationale

(1) Better Pricing

In insurance, ‘risk x exposure = expected loss’ . The acquisition of Metromile augments LMND Car with algorithms for assessing risk, tracking exposure, and pricing to expected loss. Two thirds of the population drives less than average, and the riskiest 5% are tenfold as likely to crash, but most insurers can’t tell who is who. Metromile is able to identify low-risk drivers with unrivaled precision and offer savings commensurate with their reduced risk. LMND’s acquisition of Metromile would allow for better pricing of its auto insurance products.

(2) Risk Flattening

The most vulnerable time in the life of an insurance product is during its early years, before data accumulate. Being able to minimize or bypass that stage entirely makes for a smoother ride to the top. That means more than getting there faster, it means incurring less risk, and expending less cash, along the way. LMND’s acquisition of Metromile would allow LMND access to Metromile’s data in better matching its rate to risk, thereby driving down their loss ratio.

The acquisition of Metromile was well received by the street. Stock popped ~+16% on news of the definitive agreement.

Key commentary from LMND’s co-CEO Daniel Schreiber regarding the acquisition:

“I think Metromile shortens that tremendously, and that's really the overarching thing. If you think about the strength that LMND brings to car insurance -- the product, the design, the marketing, the bundling -- we've got tremendous assets that I think give us a huge competitive advantage. But we lack the heart, which is pricing and underwriting insurance for car with precision. If you think about Metromile, they're almost the mirror image of that. They don't have bundle-able products. Their marketing has been OK. But this is what they are: They are a data science company focused on car insurance. You combine the two, you end up with something pretty powerful, that at least is the theory. You layer on top of that the fact that they've got a quarter of a billion dollars in the bank, 49 state licenses, an incredible skilled workforce, and you just see the value of the deal accruing, I think, in a way that is extraordinary.”

“What Metromile has done in a way that I think is unmatched, certainly in the United States, possibly worldwide, is they said, we're not interested in credit score correlations to driving. We want to get down to the most granular level we can. We want to be able to price at the level of one mile driven by this person, and then you can aggregate it up. But we want to get down to really granular pricing, looking at how much you drove, how you drove, getting granular data at several hertz -- so multiple times a second, they are polling their technology to see whether you're driving, where you're driving, what time of day you're driving, how you're driving, all that stuff. That creates just an incredible, detailed, textured map of what represents what kind of risks. It's invisible to the incumbency entirely. They haven't been pricing this way, they don't have these datasets, they can't price at that level of precision.”

As of today, global auto insurance market size stands at US$652bn. The market is expected to grow at 8.7% CAGR from FY23-30 to ~US$1tn. The primary drivers of auto insurance demand includes (1) implementation of strict government rules for purchase of auto insurance, (2) increase in automotive sales from rise in consumer per capita income, (3) introduction of driverless vehicles leading to safety concerns, (4) tech disruption from Insurtech players, and (4) rise in demand for third-party liability coverage in underpenetrated states and regions.

Key Operating Metrics

Premium per customer (PPC) refers to the average annualized premium customers pay for products underwritten by LMND. In layman, it refers to the average revenue per customer.

PPC = IFP / No. of Customers

In force premium (IFP) refers to the aggregate annualized premium for customers.

IFP = No. of Customer x PPC

I view no. of customer as the volume lever and PPC as the pricing lever. Volume growth to be driven by expansion of product offerings into new states. Pricing growth to be driven by cross and upsell from renter insurance into autos, pets, and homebuyer insurance.

Annual dollar retention (ADR) refers to in-force premium retained over a twelve-month period, inclusive of changes in policy value, changes in number of policies, changes in policy type, and churn. In layman, ADR measures LMND’s ability to retain customers.

Competitive Advantage

(1) LMND’s AI streamlines the insurance value chain

I view LMND as a market leader in the Insurtech space where LMND leverages on their data capabilities and easy-to-use customer facing applications in capturing the Millennial and Gen-Z first-time insurance purchasers. LMND is unencumbered by legacy systems. The company uses AI to disrupt the insurance value chain from product development to pricing and underwriting, to sales and distribution, claims management, and policy administration, essentially redefining the insurance value chain in a single integrated software stack. In layman terms, LMND i) is able to serve customers with limited human interaction, ii) at accelerated service times, iii) while pricing products accurately, thereby establishing a direct channel allowing for cheaper insurance products. The LMND experience is analogous to younger tech-savvy investors using Robinhood for investing vs. using a human brokerage firm.

(2) User-stickiness drives cross and upsell opportunities

As customers age, and their insurance needs grows, LMND can cross and upsell insurance products from their monoline business offering. Many of LMND’s customers are first-time insurance buyers, primarily in renter policy, which allows for the company to grow as these customers graduate into big ticket item insurance buyers. The ideal scenario for LMND here is to first acquire young first-time insurance buyers in renter policies. As these insurers progress in their life, they are likely to purchase bigger ticket items such as a house or a car, which means demand for housing and car insurance. Importantly, the cross and upsell opportunities come at zero additional cost of acquisition. Should this ideal scenario play out, LMND would undergo meaningful expansion on margins and return on invested capital.