Marvell (NASDAQ: MRVL)

Jul-23

Marvell is no doubt an AI beneficiary where electro-optics and custom ASICs sales can meaningfully drive topline (if executed well). However, present day risk on the stock is highly probable and can easily break the AI thesis. Valuation today is also rich where stock is trading above +1SD. An opportunity for a tactical short.

Business Overview

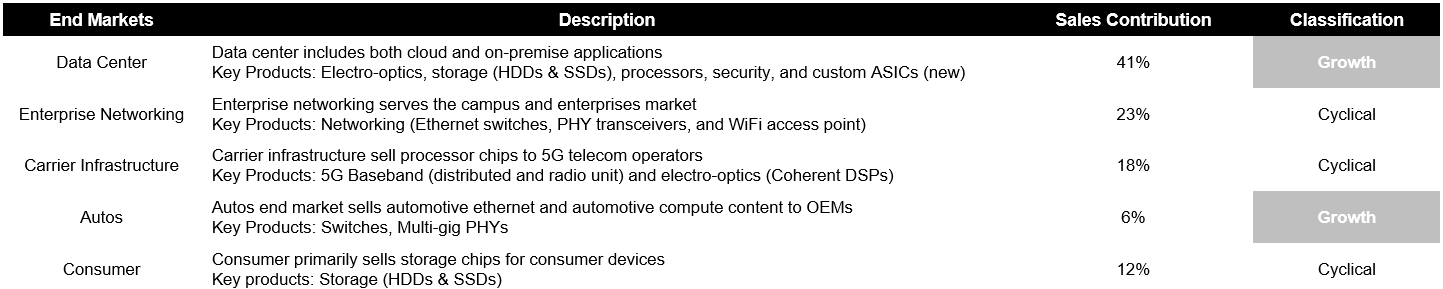

This is a complex business with 5 end markets and 6 broad categories of product lines with multiple overlaps. Below is my attempt in dissecting and explaining their business in a layman manner.

Marvell is a fabless chip designer in data infrastructure. They design chips for moving, processing, storing, and securing of data for enterprises and hyperscalers. Marvell is essentially in the data movement business, moving data between and across applications. The simple and intuitive way is to think of them as the FedEx for data. The same way Fedex moves parcels in the real world, Marvell moves data in the electronic world

The company breaks down revenue across 5 end markets. Data center is the largest today at 41% of total sales, followed by enterprise networking at 23%, carrier at 18%, consumer at 12%, and autos at 6%.

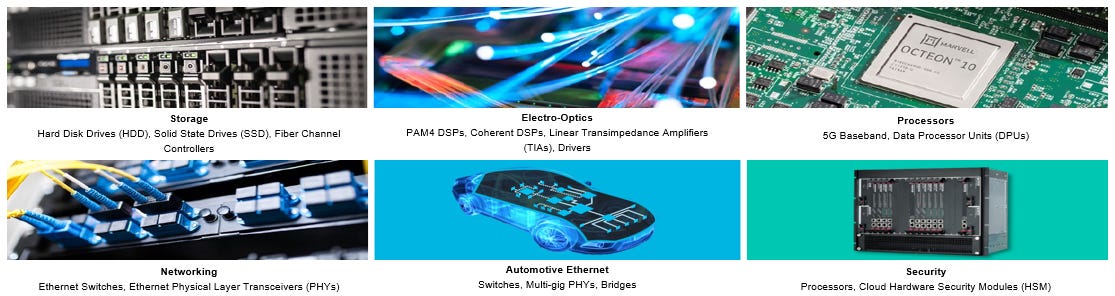

Marvell has 6 key product lines – storage, electro-optics, processors, networking, automotive ethernet, and security.

Storage are mainly controllers for hard disk drives and solid state drives. Electro-optics products essentially converts digital data from electron to photon, vice versa. Processors, specifically for 5G base station, converts digital data into radio frequency signals which can then be transmitted over a radio access network. Networking mainly consists of your ethernet switches, wifi routers. and physical layer transceivers. Networking in layman terms is simply to connect multiple devices onto a network together such that they can all communicate in a coordinated fashion. Automotive ethernet is also similar to networking. The only difference here is that you are connecting components within a car using a wired network. And then security is basically chips for data security. These modules help safeguard and manage data via encryption functions.

Marvell actually has a lot of product crossover across different end markets, so many moving pieces here. I would broadly breakdown this company into 2 main chunks, the secular growth segments and the cyclical segments.

On a product level, electro-optics and automotive ethernet are the growth portion. Storage, networking, processors, and security are the cyclical segments.

On an end-market level, data center and autos are the growth portion, enterprise networking, carrier infrastructure and consumer are the cyclical segments.

Growth Drivers

2 growth drivers today

Tailwinds of AI to drive high double-digit growth on electro-optics

Autos ethernet a growth optionality

Electro-Optics 101

Lets address the elephant in the room... WTH is even an electro-optics?! How does Marvell comes into the picture? How do they make money out of electro-optics?

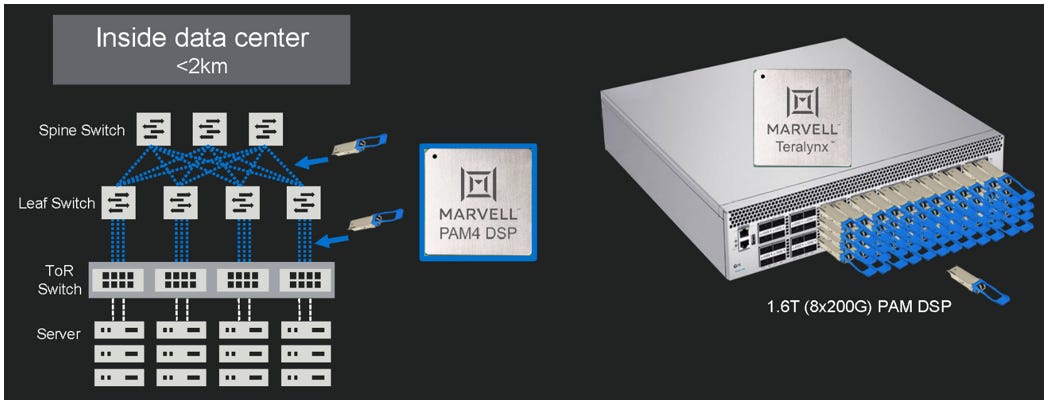

Electro-optics modules convert digital data from electricity (electrons) into light (photons), vice versa, to moving data within and between data centers.

Photons are lighter than electrons. This is why light can travel faster while consuming less energy in fiber-optics vs. electricity in copper cables.

The electro-optics module is also called an optical transceiver. Within the transceiver, is a digital signal processor (DSP) chip that does the electrical/optical signal transmission.

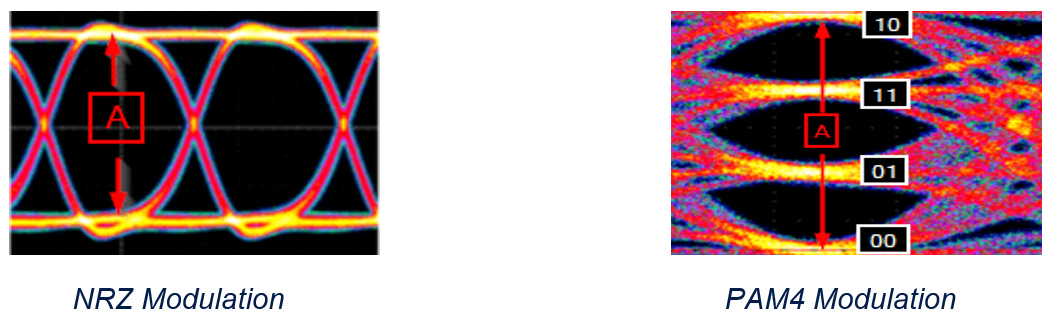

There are many types of modulation techniques for electrical/optical signal transmission. The current industry standard runs on Pulse-Amplitude Modulation 4 (PAM4).

Marvell is the dominant market leader in electro-optics with >75% market share in PAM4 DSPs. 2nd and 3rd largest players are Broadcom and Cisco respectively, each with less than 10% market share.

So in terms of how you use the module. Basically there are optical fiber wires connected to the module. The module gets plugged into the ethernet switch. That is how the connection works. These connection holes are called interconnect ports. Once the connection is linked, the module will facilitate the conversion of digital signal to light signal.

Inphi: The Game Changer

At this point, most of you must be thinking to yourself, How did Marvell ended up with 75% market share…

Marvell is where it is today because of an acquisition that they made. The original guy who had 75% market share in PAM4 DSPs is Inphi. Marvell acquired Inphi back in 2021, that’s how they ended up being the market leader.

And on how Inphi got to where they were, this was a function of its founder’s vision. Before PAM4, the industry was running on a legacy standard of data modulation technique called NRZ, or PAM2. And this has been the industry standard for the longest time since the 1990s.

Sometime around 2012/13, Inphi’s management, specifically Ford Tamer the CEO and Loi Nguyen the founder, saw limitations of NRZ as the global internet traffic accelerated. They basically said that at the rate the global internet traffic is growing, the industry will need DSPs that can transmit data at a much higher rate, beyond 100G. NRZ had a limitation of 100G. To go above and beyond, we need to change the modulation technique from PAM2 to PAM4. And this led to Inphi spending aggressively on R&D in developing PAM4 capabilities while the rest of the industry only competed in NRZ products (as they saw no room for PAM4 commercialization).

For the longest time, Inphi wasn’t profitable. 2012 to 2017 they always had one of the lowest absolute sales figure relative to peers. Gross margin was actually decent but their operating margins remained negative. This was because of the R&D that they have been spending in developing PAM4. As a % of sales, R&D has always been above 40%. I allude the capital allocation into R&D as a key factor that ultimately positioned them with over 75% market share. By 2020, everyone realized they couldn’t go further than 100G with NRZ, they needed PAM4. At that time, Inphi was the only player with PAM4 DSPs. That explains revenue doubling from 2019 to 2020.

Tailwinds of AI driving high double-digit growth on electro-optics

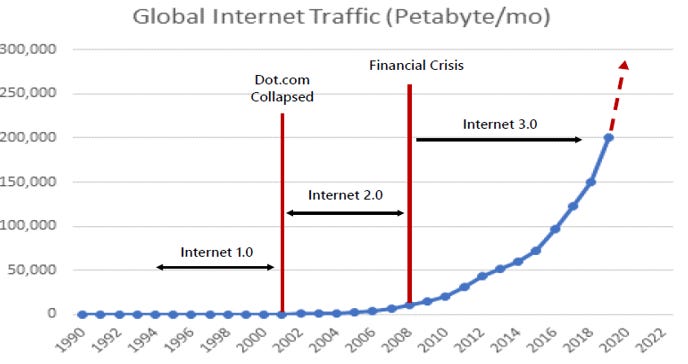

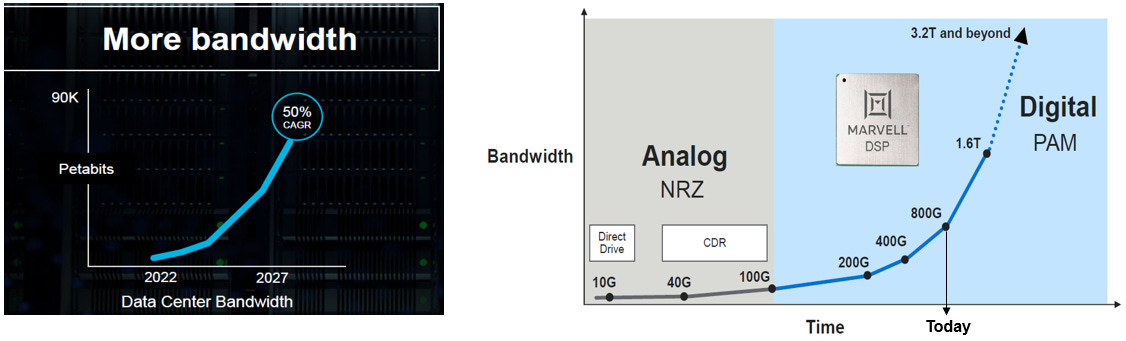

As we progress from the pre-covid to the post-covid era, internet traffic has further accelerated due to a confluence of reasons such as zoom calls when we work from home, short form videos from social media platforms like tiktok, and generative AI as a new way of using internet. All these applications are driving higher data traffic, which in turn is driving higher network bandwidth requirements. In layman terms, what it means is that the maximum amount of data that is transferred over a network connection is increasing exponentially. Effectively, data center industry growth today is driven by growth in network bandwidth where it is currently growing at a 5-year CAGR of 50% through 2027. This exponential expansion in data requires better, faster, and more efficient DSPs.

As of today, hyperscalers are in the upgrade cycle of transitioning from 400G to 800G, and 800G to 1.6TB PAM4 DSPs. Importantly, given the speed at which AI infrastructure is advancing, the upgrade cycle is now cutting down from the traditional timeframe of 4-5 years to under 2 years.

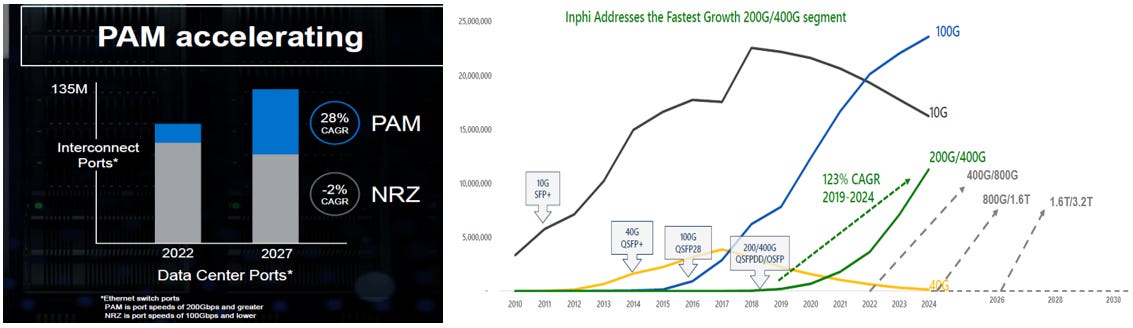

On pricing, every upgrade cycle i.e. 200G to 400G or 400G to 800G, raises ASP by +10-15%. On volume, we can expect ~28% growth through 2027 – this is based on growth in interconnect ports. Volume growth in transceivers should be in line with volume growth of interconnect ports since transceivers are plugged into the interconnect ports.

Marvell in its most recent quarter, disclosed their AI revenue for the first time. They did $200mn of AI revenue last year. Guiding for $400mn this year, followed by $800mn next year. While stock has reacted on the guided AI revenue, I believe street has yet to price in the magnitude of growth from electro-optics beyond FY25E. I am of the view MRVL can sustain above 20% growth till end of the decade due to its market leadership in PAM4 DSPs. As mentioned earlier, MRVL has >75% market share in PAM4 DSPs. Importantly, they are always the first to rollout the latest PAM4 product to the market, 1-2 years ahead of any customers and competitors’ roadmap. This effectively positions MRVL as the go to supplier of PAM4 solutions. MRVL’s ability to maintain above 75% market share with no signs of share loss in the last 8 years ultimately gives me comfort and confidence that they can sustain above 20% growth on electro-optics revenue till end of the decade.

Overall, I would say Marvell’s PAM4 DSPs is really the crown jewel for the company today. It’s the one and only asset that is positioning long-term secular growth for Marvell today.

Autos Ethernet a growth optionality

Beyond electro-optics, there is a growth optionality coming from autos ethernet. I view this as a “call option / optionality” as the earliest possible time for this to play out is at least 3-4 years out.

Autos ethernet SAM today is driven by growth in automotive ethernet port shipments on the volume side, and ethernet dollar content per car on the pricing side. On the volume side, Marvell sees automotive ethernet port shipments growing at 39% CAGR. On the pricing side, ethernet content per car is growing from under $10 per car to about $50-70 of ethernet content per car.

Net-net, Marvell estimates that the Automotive Ethernet market could be the next $1bn Ethernet IC market and they are targeting 50% share in this market over time. Revenue contribution for this segment today is around 6-7% of total revenue, been growing at high double digit for the last 2 years. I think this segment will only start to garner interest from investors when contribution surpasses 10%. I am modelling high double digit growth for this segment over the next 3-4 years. Sales contribution should surpass 10% sometime in 2026 or 27. Still a few years out before this segment can contribute meaningful growth to topline.

Where I differ vs. The Street

To be clear, I’m bear on Marvell. I’m not a fan of it, hear me out…

While Marvell can be a meaningful AI beneficiary with exposure to electro-optics, current valuation is rich, and the stock faces meaningful risks on the horizon. I am of the view that the stock is not actionable at current levels.

3 Key Risks

Inventory Correction (Near-Term)

Custom ASICs (Long-Term)

Alternative Technologies to PAM4 DSPs (Long-Term)

Inventory Correction

Unlike Broadcom, Marvell is poor in managing lead time, hence very susceptible to major inventory correction. This explains the volatility of Marvell’s stock price relative to other fabless players. I would also think that LOs generally prefer Broadcom over Marvell and that this is a stock mainly played by the HFs.

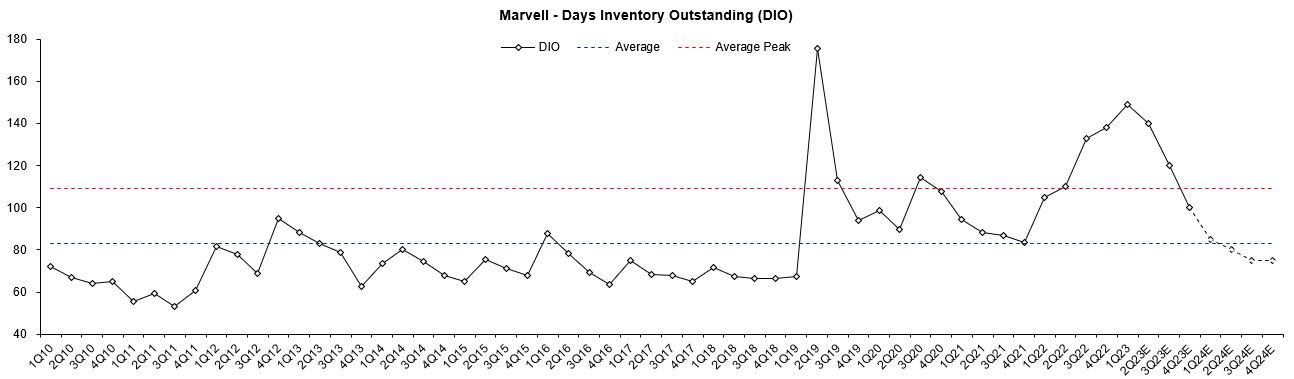

Marvell is undergoing correction in 2 of their end markets - (1) storage, and (2) enterprise networking. Going by my estimates, DIO will continue to stay elevated for another 2 to 3 quarters before returning to normalized levels.

For storage, data center has bottomed out in FY1Q24 to ~$80mn vs. historical average of ~$120mn. Going forward, I expect flat to low single digit sequential growth in FY2Q24 and FY3Q24 before more meaningful growth can be felt.

For enterprise networking, this segment has just begun its inventory correction where managment is expecting end market “to decline by more than 10% sequentially”. This marks Marvell’s first quarter of decline.

The above chart illustrates Marvell’s DIO in the last 13 years. Typically, inventory correction lasts for 2-3 quarters before normalizing. AS of today, storage has bottomed out but enterprise networking has just started its digestion. This cycle’s correction will take at least another 2 quarters before returning to under 80 days in my opinion.

Custom ASICs

A quick introduction on custom ASICs before diving deeper into how it serves as a risk to Marvell…

Today, most applicatoins run on general-purpose GPU chips. These chips are one size fit all product, they are expensive, and not optimal in terms of performance and energy when it comes to AI applications. You can think of general-purpose GPU as a chip that is jack of all trades, but master of none. In the context of AI, one does not need the chip to perform multiple functions well, but rather the ability to perform only one function and be the very best in it. There is hence a new wave of demand for customization and optimization of applicatoin sepcific chips known as custom ASICs. While Nvidia sells AI chips, their strong bargaining power makes these chips ridiculously expensive. Hyperscalers today hence requires vendor diversification. This explains why hyperscalers are co-designing their AI chips with fabless designers. As of today, Google and Meta are getting their AI chips from Broadcom. AWS is getting their AI chips from Taiwanese custom ASICs pureplay, Alchip.

There is a bull debate on custom ASICs where this could be a new growth engine for Marvell. According to sellsdie estiamtes, SAM today is growing at 4-years CAGR of 85% from US$2.5bn in CY23E to $29bn in CY27E. Custom ASICs is currently a small revenue contributor for Marvell, under $200mn (<1% of total sales). Management in recent quarters has turned incrementally positive on this segment and now expect to deliver more than $800mn of topline within the next 2 years.

For context, Broadcom’s custom ASICs revenue from co-designing Google’s TPU chip grew at a 6-year CAGR of 98% from US$50mn in CY17 to over US$3bn in CY23E. In terms of sales contribution, it went from < 1% to ~8% of total sales in CY23E. Given Marvell is in works to secure Amazon in co-designing their Trainium AI chip, this is giving Street a good sense of direction and plausibility on how significant Marvell’s custom ASICs revenue could growth into in 4-5 years time. The Street is essentially betting on custom ASICs as a new growth engine for Marvell.

I take an opposing view to the bull debate on custom asics. I see a high barrier for Marvell to win in custom asics due to competition from Taiwanese custom ASICs pureplay, Alchip. On competition, it has been rumored that Marvell has been facing execution problems in co-designing AWS's Gen 3 Trainium chip. Its also been rumored that Alchip is competing against Marvell to secure AWS's Gen 4 Trainium chip.

Alchip appears to have more rights to win than Marvell. Reason being, Alchip can offer lower price with faster delivery time. On pricing, Alchip's gross margins historically has always been in the low 30s, they definitely can offer a price lower than what Marvell would be willing to go down to. On speed, Alchip has close ties with TSMC. This allows Alchip to design and deliver the chips much faster than most fabless players out there. The same can’t be said for Marvell.

If Alchip does win this contract from Marvell, I would expect consensus estimates to cut back on Marvell's topline for 2025 and 2026, multiples will likely derate significantly. Easily, we would see a huge impact of share price correction. Also, the margins for custom ASICs is pretty low at 30-35% relative to Marvell's gross margin of 62%. So even if Marvell does secure the chips, we very well could see some dilution on gross margins. Net-net, either outcomes seems to be negative for Marvell.

Alternative Technologies to PAM4 DSPs

Back in Mar-23, a Chinese player, Eoptolink, came out in an optics conference to announce a new technology called linear direct drives. In this architecture, there isn’t a need for DSPs. This sparked fears of LDD displacing DSPs, effectively wiping out the need for Marvell's PAM4 DSPs. As mentioned earlier, Marvell has 75% market share in this space. If the industry starts adopting LDD, there is a good chance of Marvell losing share and essentially losing their edge.

The near-term mitigation here is that, Marvell's DSP has advantages of standardization, flexibility, and upgrade roadmap far outweighs the value add from linear think its hard to quantify the overall impact today, but I would at least expect some form of multiple derating if the industry starts adopting the LDD solutions.

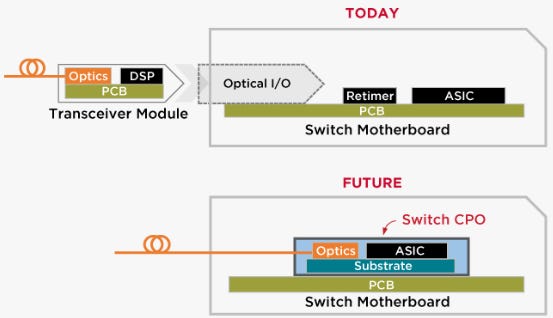

Another alternative technology to PAM4 DSPs is co-packaged optics. How this technology works is that instead of using the module where you insert the plug into the interconnect port to link it to the switch. The chip gets directly implanted into the switch motherboard.

One key driver of adoption for CPO is power. Power consumption is critical in data centers as it limits what kind oftechnology can be built and deployed. What’s happening today is that, as we upgrade the speed of the optical transceivers, the power consumption increases exponentially. By using CPO, one can reduce the distance of connection between the switch and the optical input/output, and this saves up to 30% of power.

The near-term mitigation for PAM4 DSPs pluggables today is its low switching cost relative to a CPO. When a transceiver fails, all you need to do is to replace it with a new one. But for CPO, it is installed inside the switch, you’ll need to replace the entire switch set.

I do think risk #3 poses significant existential risks to Marvell hence my discomfort on the company’s long-term positioning as a market leader in PAM4 DSPs. Importantly, as I’m writing this piece of noob research, NASDAQ:CRDO is taking share from Marvell in 800G…

Valuation

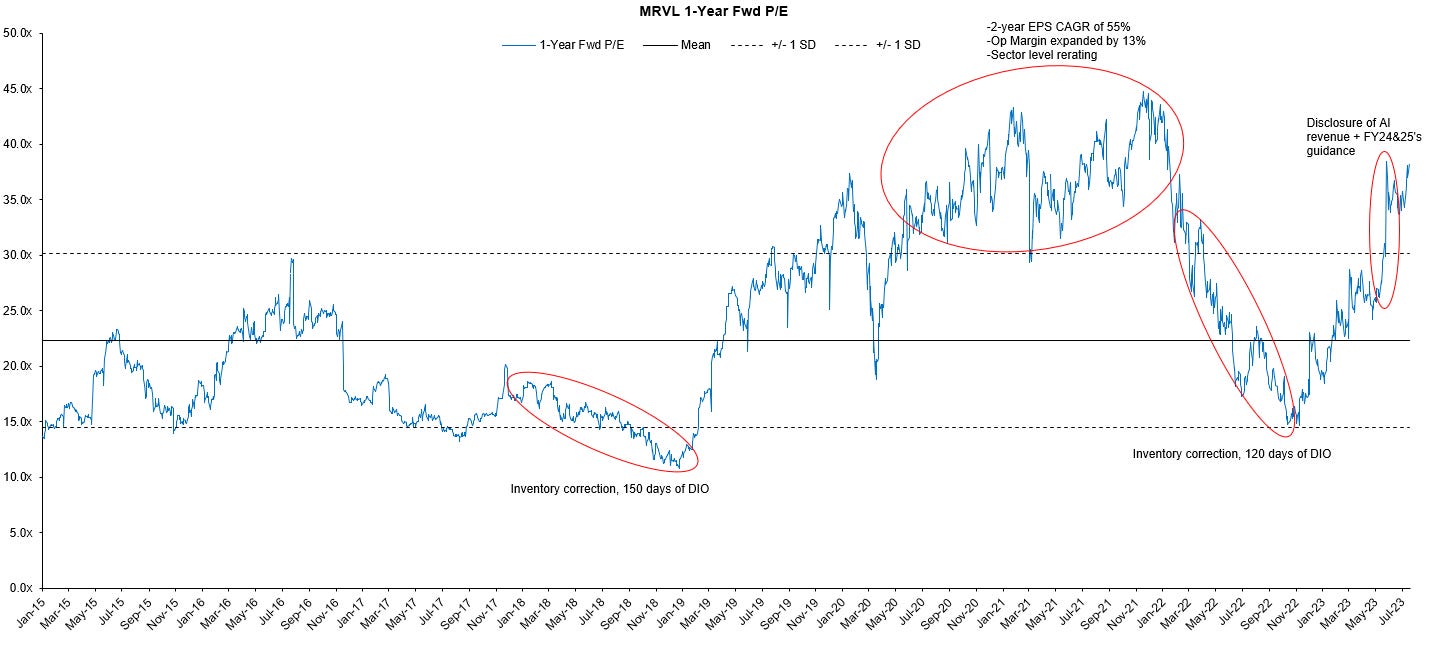

Stock is expensive today, trading above 1SD at 35x 1-year forward earnings. In times of inventory correction, stock tend to derate down to-1 SD. I triangulated Marvell's valuation across a few methodologies and time frame, and am getting a range of -2% to +24% upside. On a blended basis I am getting +7% upside from current stock price.

Historically, the company grew at a 7-year CAGR of 13% on topline. I am assuming 10-year CAGR of 11%. Consensus estimates is only expecting 5-year CAGR of 6.6%.

I ran a reverse DCF, assuming 36% operating margin, market is implying topline growth at a 10-year CAGR of 15%. Clearly, market is baking in huge Al growth on Marvell. My take is that Marvell deserves to trade at some premium due to Al exposure. An appropriate range is within the +1SD range rather than above it. Should my risks materialize, I would expect ~30% downside from current levels.